-

-

-

PT | EN

PT | EN

PT | EN

The centers of global power are shifting at an unexpected pace. Hegemonies perceived as immutable are giving way to new poles of production and consumption. By 2025, the relative decline in the renewal capacities of the United States and Europe coincides with the return of the world's economic engine to Asia. ASEAN stands out in this new reality as an ambitious innovation platform and an important consumer market. In a scenario of geoeconomic transformations, marked by the unpredictability of the political and commercial actions of traditional hegemonies, Brazil has much to gain by investing in deepening its rapprochement with Southeast Asia.

Because without the United States, everything in the world would die.

It´s true. It´s so powerful. It´s so big.

– Donald Trump, entrevista à imprensa na Casa Branca, 3 de setembro de 2025

Instead of inquiring why the Roman empire was destroyed,

we should rather be surprised that it had subsisted so long.

– Edward Gibbon, History of the Decline and Fall of the Roman Empire, Volume VI

Le monde a changé, il doit changer encore.

– Maximilien de Robespierre, Discours du 18 Floréal, An II

"The truth is that there were only great powers in Europe, and today they are the first to recognize that there is in the New World a great and powerful nation with which they must reckon and which necessarily must have its share of influence in the international politics of the whole world" (Lins 1995, 318). Thus spoke the Baron of Rio Branco in 1905, in a dispatch to the newly inaugurated Brazilian embassy in Washington. The civil war that pitted the industrialized North against the rural, slave-owning South had already ended 40 years earlier, and the United States appeared on the international scene as an increasingly imperial economic power, supported by steel, oil, railroads, manufacturing, urbanization, and rapid social transformation. Rio Branco "did not miss the vision of this phenomenon, which was that of international power being divided, at the end of the 19th century, between Europe and the United States," recalls Álvaro Lins (1995, 317) in his classic biography of the Brazilian chancellor.

Not all foreign policy makers at that time possessed the same foresight. The Argentine legation in the US capital, which, like the Brazilian legation, had been operating since 1824, would only be elevated to the status of an embassy in 1914. Without neglecting its relationship with Europe, at the beginning of the 20th century, Brazil decided to present itself as the main South American interlocutor with the US, seeking to consolidate its regional visibility and expand its international projection. Argentina, on the other hand, chose to continue prioritizing its insertion into a European system anchored primarily in the United Kingdom, which it insisted on perceiving as the central axis of the international framework as a whole. It can be argued that this contrast was decisive in shaping the subsequent geopolitical orientations of the two countries and had long-term effects on their respective economic development processes.

Argentina's strategy of prioritizing its traditional ties with Europe, to which it exported its agricultural products and on whose capital and markets it depended, would continue to bear fruit for another couple of decades, certainly until the 1930s. In the mid-1940s, however, the Brazilian economy, by investing in the development of its industrial base[1] within an economic framework centered on the United States (US), surpassed the Argentine economy for the first time, weakened by the disaster of the two great European wars. From then on, the neighboring country would no longer manage to overcome its relative economic decline in relation to Brazil, which would consolidate itself as the largest economy in Latin America and, since the mid-1970s, as one of the largest in the world.

However, shifts in the world system's center of gravity happen with surprising speed.

At the end of 2025, we are a long way from 1991, when the spontaneous dissolution of the Soviet Union inspired the mirage of an end to History[2] that would ensure the preeminence, as far as the eye can see, of Washington's perspective on the course of the international scene. Paradoxically, it was from that moment of apparent triumph that the normalization of practices was established, which, over the following decades, would generate serious, concrete limitations for the victors of the Cold War's economies. Policies of deregulation, deindustrialization, widespread privatization, reduction of taxes on capital and a focus on financial capitalism to the detriment of the real economy would contribute to the concentration of income, the abandonment of investments in physical infrastructure and the important and undeniable relative impoverishment of the middle class[3] in the United States.

We are now a long way from 2001, when, upon joining the World Trade Organization, China embarked on a lightning-fast process of integration into the global economy–of which it became the key player–and, at the same time, the formation of a gigantic domestic middle-class consumer market. The consequences, for China itself, Southeast Asia, the so-called Global South, and the world, would be profoundly transformative.

The United States' share of global trade in goods, which peaked in the post-war 1940s at about one-third of the total, and still accounted for about 25% in the 1970s, began to decline significantly from the 1980s onwards, as the international rise of the Japanese and West German economies took hold. Despite the success of the US strategy of containing German and Japanese competitiveness[4], the US continued to lose ground through a gradual but continuous disengagement from the global economy. Its degree of trade openness, measured as imports and exports relative to GDP, has not kept pace with the global trend. The unprecedented pace of China's incorporation into global value chains and the 2008 financial crisis accelerated this contraction[5]. In the current reality of global trade in goods, estimated at US$ 50 trillion by 2025, the US exports US$ 2.12 trillion and imports US$ 3.15 trillion. China exports US$3.63 trillion and imports US$2.63 trillion. The United States, therefore, accounts for 10.6% of global trade in goods, while China leads with 12.5% (World Trade Organization 2025; UNCTAD 2025)[6].

In terms of industrial capacity, China surpassed Japan in 2005, the US in 2008, and the European Union in 2011. Recent World Bank data suggests that China's industrial capacity is approaching the combined capacity of the United States, the European Union, and Japan[7]. This trend shows no signs of reversing in the short- or medium-term. The usual caveats maintain that, although the volume of Chinese manufacturing output is unparalleled, the US and Europe are still ahead in high-value innovation. In practice, the increase in Chinese exports of high-tech goods (electric vehicles, industrial robots) and China's recent progress in the semiconductor industry demonstrate its leadership in technological innovation. Sanctions on exports to China of critical technologies related to chip production have accelerated Chinese domestic development in this area (Huawei, SMIC), signaling increasing autonomy from Western inputs. As the world's largest consumer market for technology, China is also a critical source of inputs and raw materials, dominating numerous global supply chains, from rare earths and lithium-ion batteries to solar panels and high-precision optical components.

The United States has been losing ground in innovation, partly due to reduced federal funding for research and development (R&D), which reportedly fell from about 67% of all domestic R&D in 1964 to less than 20% in 2023, according to the National Science Foundation (2025). The American share of scientific output and engineering fields has been gradually declining, in parallel with China's rise in this domain. According to the World Intellectual Property Organization (WIPO), China has led in the annual number of patents granted since 2011 (WIPO 2024). In 2023, it held approximately five million patents in force, compared to approximately 3.5 million in the US (WIPO 2024). Although this indicator is not, in itself, synonymous with technological vanguard, China has established itself as a global champion in applied innovation–driven by its market scale, industrial execution capacity, speed of technological diffusion, sectoral leadership, rapid learning cycle, and growing power to set standards–surpassing Western economies in several key segments.

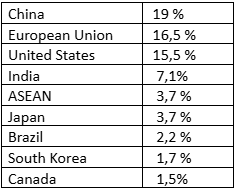

The International Monetary Fund's (IMF) October 2025 World Economic Outlook report indicates that, with regard to the global economic weight in purchasing power parity (PPP), the United States now accounts for no more than 15.5% of global GDP, with a trend toward contraction; the European Union, 16.5%, with a trend toward contraction; and China, approximately 19%, with a trend toward expansion (IMF 2025).

Table 1 – Share of global GDP in PPP/2025. Source: WEO (2025).

The same source indicates that the weight of the Global South–which we will understand here as Emerging and Developing Market Economies (EDMEs)–added to China's weight accounts for 60.64% of global GDP in PPP in 2025. Subtracting China's share from the Global South, we arrive at 41.64% of the total, which is still a larger proportion than the combined presence of the US and the European Union (32%). If we consider the combined presence of the United States and the EU, plus Canada, Japan and South Korea (a group that we could roughly refer to as the Global North), the total in GDP/PPP would reach 38.9%, that is, still less than the combined weight of the Global South without China.

Table 2 – North vs. South: share of global GDP in PPP/2025. Source: WEO (2025).

IMF data demonstrate that we are facing a historic reversal in the engine of economic power and reveal a profound structural change. The Global South, excluding China, already surpasses the Global North in GDP/PPP, outweighing the economies the IMF still refers to, with unintentional irony, as advanced economies.

One hundred and twenty years later, the US, a rising power in 1905, is now experiencing an undeniable relative decline in its share of global trade, industrial production, scientific and technological output, and world GDP. Its monopoly on military power is no longer certain either. The Chinese military parade on September 3, 2025, which marked the 80th anniversary of the victory over Japan in World War II, was considered by expert observers[8] a critical milestone in China's mastery of technologies that rival or surpass those of the United States[9]. The United States, which was an unavoidable actor until recently, now accounts for only about 13% of Chinese exports (UNCTAD 2025) and absorbs less than 12% of Brazilian exports (MDIC 2024).

The world has changed. The 20th century, the so-called American century, ended a quarter-century ago. We are no longer in a moment of transition, but in a moment of post-transition. The re-emergence of China as a power has established a new commercial dynamic in a transformed global economic reality.

As in 1905, the signs are more than clear. Reputable conservative sources, such as those cited here, confirm that a systemic reconfiguration has taken place, a shift in the center of gravity of global economic power. What is remarkable is that it is necessary to state what is evident, and that, in doing so, this may generate incredulity or arouse sensitivities. In the conventional discourse of the academic intelligentsia and Western opinion leaders, the dogmas of American exceptionalism and European centrality, and the desired collapse–always presented as imminent–of China's capacity for sustained growth, continue to be recited today, as they have been for the last 30 or 40 years.

In his memoirs on the Sino-American rapprochement of 1972, Henry Kissinger wrote that China under the last imperial dynasty (1644-1912) entered the modern era dominated by a political elite "oblivious to the onset of the Western age of exploration" and "unaware of the technological and historical currents that would soon threaten its existence." At the time, according to Richard Nixon's Secretary of State[10], there was no shortage of currents arguing that it was necessary to counter European advances by strengthening internal capabilities and adapting technologically. Supported by a conservative population, the prevailing faction, however, decided that adapting would be tantamount to abandoning the essence of Chinese heritage, which was perceived as invincible. "Centuries of predominance," he concludes, "had warped the Celestial Court's sense of reality" (Kissinger 2011, 49-63).

Whether due to ideological conditioning or cognitive inertia–as was the case on the eve of the capitulation to the British invaders by the courtiers of the Qing dynasty, like the Argentine elite in the 1910s–the still predominant Western analyses tend to privilege dogma over factual evidence, clinging to a past that is already gone.

China's economic rise has transformed the balance of power in world trade. One effect of this transformation has been an increase in trade among actors in the Global South. By importing large volumes of raw materials and exporting affordable manufactured goods, Chinese expansion has not only increased bilateral trade between its own market and other developing markets but has also fostered new investments and trade agreements that have expanded the flow of goods and services within the South. This rise has promoted the integration of Southern economies into large supply chains, intra- and extra-regional networks, and increasingly resilient, diversified trade exchanges. Through trade realignments and the diversification of partnerships, it has produced increasing economic and commercial autonomy for the South vis-à-vis the United States and the European Union. IMF projections suggest the trend will continue, with the South's GDP growing faster than the North's[11].

Brazil, already a relevant player in this new context, has the conditions to continue adapting to the rhythm of technological and geopolitical cycles, which seem to be getting shorter and shorter, rejecting anachronistic interpretations and gathering the tools to make the best use of reality and position itself in an increasingly competitive way in the face of this new configuration.

RISE OF ASEAN

The world's economic and commercial axis has shifted to Asia. Or rather, it has returned to Asia after about 250 years during which it was exceptionally well anchored in the North Atlantic. It is in emerging Asia–China, India and Southeast Asia, extending far beyond the US tributaries Japan and South Korea–that the main source of global economic growth is found today, both in production and, with its immense markets, in consumption.

It is known that China is the main trading partner of about two-thirds of the United Nations member states; it has been, for 16 years since 2009, the country with which Brazil, for example, maintains the largest total trade volume year after year. However, the question of China's main trading partner is rarely raised.

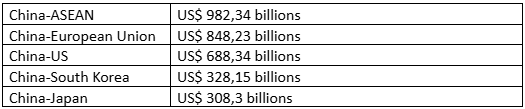

For five consecutive years, since 2021, China's main trading partner has been the Association of Southeast Asian Nations (ASEAN)–followed by the European Union, the United States, South Korea, and Japan. In 2024, the respective trade volumes were as follows (US Census Bureau & BEA 2025):

Table 3 – Data from the US Census Bureau and the ASEAN Secretariat. US Census Bureau and Bureau of Economic Analysis, "US International Trade in Goods and Services, December and Annual 2024."

ASEAN's main partner, for the 16th consecutive year, is China itself, in a deep integration that extends beyond trade to include Chinese direct investment and integration into global supply chains. The closeness of the relationship stems from the facilitation of flows of goods, services, inputs, and investments promoted by the ASEAN-China Free Trade Agreement of 2005 and the Regional Comprehensive Economic Partnership (RCEP) of 2022, which will be examined later.

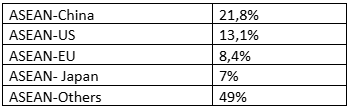

The current trade volume between ASEAN and China, exceeding US$982 billion, represents approximately 16% of China's total trade (MOFCOM 2025) and about 20% of ASEAN's total trade (2024a). The proportion of trade flows (goods) between ASEAN and its major partners, excluding intra-ASEAN trade, is approximately as follows (ASEAN 2024b, 2024c):

Table 4 – Proportion of ASEAN trade partnerships. Source: ASEAN Merchandise Trade Statistics 2024.

Created in 1967, ASEAN has been a free trade area since 1992, bringing together Brunei, Cambodia, the Philippines, Indonesia, Laos, Malaysia, Myanmar, Singapore, Thailand, East Timor, and Vietnam. Some of these economies (Indonesia, Malaysia, Thailand, the Philippines, and Vietnam) have considerable population and economic weight. Others, such as Laos or Cambodia, have shown signs of increasing dynamism. Together, these 11 countries are among the fastest-growing in the world. ASEAN's GDP has practically doubled over the last ten years and could double again over the next decade. Organized as an Association, Southeast Asia is one of the regions that has benefited most directly from the shift of the global center of the economy and trade to the East.

ASEAN is the result of remarkable success in building a regional integration structure amidst extreme diversity. Although geographically close, its members (to which Timor-Leste joined as a full member on October 26, 2025) are countries with extremely diverse languages, religions, cultures, and ethnicities. ASEAN encompasses hundreds of languages[12] and multiple religions and ethnicities. Economic disparities, such as those between Myanmar (nominal GDP per capita of just over US$1,000) and Singapore (nominal GDP per capita of US$92,000), or population density, such as between Timor-Leste (less than 2 million inhabitants) and Indonesia (280 million inhabitants), have not impeded the fluidity of political coordination and commercial integration.

The free trade area (FTA) established in 1992 used a common preferential tariff, adopted through tariff-reduction schedules, to foster intra-regional economic integration and enhance the region's competitive advantages as a production base for the global market. The FTA evolved into a broader and more ambitious vision of integration, leading, in 2015, to the formation of the ASEAN Economic Community (AEC), which established a single market with the free flow not only of goods, but also of services and investments, capital and skilled labor[13], to create an effectively integrated production and consumption platform. The ASEAN strategic plan for the 2026-2030 five-year period, known as the post-2025 Blueprint, is a natural evolution of the AEC's ambitions, focusing on digitalization, the green economy, resilience to global shocks, and the mitigation of development disparities among member states.

GROWTH PROSPECTS

In a context of accelerating economic and commercial globalization and the rapid enrichment of Asia from the 1980s and 1990s onwards, ASEAN was able to capitalize on the Asian miracle to integrate into global value chains. The regional GDP rose from about US$ 500 billion in 1990 to more than US$ 4 trillion in 2025, positioning the Association as the fifth-largest economy in the world, on par with India[14].

What was, less than 40 years ago, a collection of poor economies dependent on the export of commodities and rudimentary manufactured goods has become a diversified, highly integrated economic powerhouse recognized as one of the world's leading hubs for manufacturing, technology, and services. Successful regional integration and an emphasis on industrial development and attracting foreign direct investment have been the cornerstones of this trajectory.

ASEAN is emerging today as an Industry 4.0 platform, with a strong position in advanced industries supported by systematic and deliberate regional policies. Initiatives adopted by common agreement promote joint projects in semiconductors, electric vehicles, and biotechnology, leveraged by investments from China and Japan. The manufacturing sector accounts for approximately 30% of regional GDP, growing at around 6% per year, with a focus on electronics (Malaysia, Vietnam) and automotive (Indonesia, Thailand).

Economic growth projections for ASEAN until 2030 vary by country, but the consensus is for sustained expansion. Indonesia, the bloc's largest economy, is expected to grow at 5.1% per year, raising its GDP from US$1.4 trillion in 2025 to US$2.5 trillion in 2030, benefiting from natural resources and manufacturing. The Philippines and Vietnam, with rates above 6%, will reach US$800 billion and US$700 billion, respectively, driven by exports and foreign investment. Thailand and Malaysia project 4% to 5%, focusing on tourism and electronics, while Singapore, with 3% to 4%, maintains its leadership in financial services[15]. Countries like Laos and Myanmar, although more volatile, benefit from regional integration through the Regional Comprehensive Economic Partnership Agreement (RCEP), which I will discuss below and which is estimated to add US$1.2 trillion to intra-Asian trade by 2030.

Regional GDP growth rates are projected to reach 4.8% in 2025, exceeding the global average of 3.2%, driven by exports (approximately 40% of ASEAN GDP) and tourism (5-10%). GDP per capita has grown by 4.5% over the past decade, from US$3,500 in 2015 to US$6,010 in 2025, reducing poverty from 16% to 6-7%, despite persistent disparities among Member States.

To sustain growth in production capacity that continues to meet domestic demand and its export potential, ASEAN relies on several positive structural factors. With over 690 million inhabitants in 2025–almost three times the population of Brazil (212 million)–the Association has a young workforce, with the demographic dependency ratio declining until 2030, in contrast to the aging trend in Western economies.

Urbanization is expected to remain a key driver of growth dynamics in Southeast Asia. Between 2020 and the end of 2025, it is estimated that 70 million people will have migrated to cities, raising the urbanization rate from 50% to 60% by 2030. According to the Asian Development Bank (ADB), this trend is expected to continue, requiring trillions of dollars in additional infrastructure investments, boosting sectors such as construction and services, and increasing labor productivity.

An emerging middle class could act as a key catalyst in this process. It is estimated that the middle-class segment of the ASEAN population, which numbered 91 million in 2010, will grow to 334 million in 2030 (51% of the population). The IMF estimates that the disposable income of this sector could grow by 56% in the so-called emerging ASEAN-5 (Indonesia, Malaysia, Philippines, Thailand and Vietnam). Combined with digital penetration (92% in Indonesia's urban areas by 2030), this expansion should boost domestic consumption, which already accounts for 60% of regional GDP[16]. E-commerce and fintech services could add US$1 trillion to GDP by 2030, fostering sustained demand for consumer goods, education and health.

More than just a growing bloc, ASEAN presents itself, in short, as a resilient ecosystem where sharp intra-regional coordination, urbanization, favorable demographics, and the rise of the middle class converge to sustain growth and robust domestic consumption. Southeast Asia seems prepared to overcome its internal bottlenecks and navigate global risks, such as the new US trade tariffs, while remaining a pillar of the world economy.

ASEAN AND THE REGIONAL COMPREHENSIVE ECONOMIC PARTNERSHIP (RCEP)

The major Asian trade agreement, the Regional Comprehensive Economic Partnership (RCEP), brings together, in addition to ASEAN, China, Japan, South Korea, Australia, and New Zealand, a total of 16 economies. The RCEP was signed in November 2020 and has been in effect since January 2022. Covering 30% of the world's population, 30% of global GDP, and 28% of international trade, the RCEP is the world's largest trade agreement.

ASEAN played a key role in the success of the negotiations, which spanned from 2012 to 2020, acting as the central coordinator from the outset. The RCEP evolved from bilateral initiatives ASEAN+3 (China, Japan and South Korea) and ASEAN+6 (with the entry of India, which would withdraw from the negotiations in 2019[17], Australia and New Zealand), with the definition of the agenda and rules of engagement always remaining the responsibility of ASEAN. The use of its characteristic diplomatic methodology–the so-called ASEAN way, based on consensus, flexibility and inclusive negotiations–streamlined the process by centralizing decisions, reducing duplication and ensuring that negotiations progressed in annual rounds under the Association's rotating presidency.

The RCEP provides States Parties with, among other benefits, the elimination or reduction of tariffs, cumulative rules of origin known as "diagonals," investment facilitation, and standardization of digital trade. The agreement eliminates or reduces tariffs on more than 90% of goods within 20 years, with extended deadlines for least developed countries (up to 25 years for Cambodia). Its diagonal rules of origin, based on 40% regional value added, allow inputs from any State Party to be counted towards preferential qualification. Investment facilitation is conducted through negative lists (automatic liberalization except for explicit reservations), prohibition of performance requirements (such as mandatory technology transfer, with transitional exceptions for least developed States Parties), and standardization of digital trade, with provisions on cross-border data flows and protection of personal information, without forced server localization by default. Customs facilitation aligns with the WTO Trade Facilitation Agreement, with goods cleared within 48 hours, equivalent to an additional 9% reduction in non-tariff barriers.

From ASEAN's specific perspective, the RCEP strengthens intra-Asian production and trade chains, encourages increased foreign investment, and enhances the competitiveness of each of the Association's members. The integration of its smaller economies, such as Vietnam and Cambodia, into networks led by China, Japan, and South Korea, especially in electronics and automotive sectors, is particularly welcome. The agreement further enhances the competitiveness of the member states by harmonizing intellectual property standards, competition, and support for small and medium-sized enterprises through cooperation committees.

With the exception of two or three articles published at the time of its entry into force, there do not appear to be any objective, comprehensive, and above all continuous analyses over time in the West on the effects of what is, in concrete terms, the world's largest trading instrument and the first in History to bring together China and Japan.

The scant press and think tank coverage of the new agreement tends, with a single instinct, to cultivate negative bias, emphasizing perceived deficiencies such as the absence of more robust clauses on intellectual property. Much criticized is the supposed lack of ambition in the tariff area, which is natural, however, in a commercial environment where, thanks to the pre-existing network of ASEAN FTAs (with China, South Korea, Japan, Australia and New Zealand, and among the member states themselves), the cuts affect an already low tariff base, consolidating reciprocal advantages previously granted between the Parties.

The fact that a trade arrangement larger than that of the European Union, in effect for almost four years, tends to be ignored or minimized by expert observers reflects the reverence with which the sensitivities of the Celestial Court of our day are still regarded. The fact that the United States' historical partners in Asia–Japan, South Korea, Australia, and New Zealand–have joined the RCEP does not encourage professional commentators to admit that we are facing a watershed moment in Asian integration, whose innovative impact goes far beyond tariff and intellectual property issues.

Comprising the gigantic economies of China, Japan, and ASEAN itself, and encompassing e-commerce, competition, government procurement, harmonization of rules of origin, customs facilitation, trade facilitation, and supply chain integration, the RCEP has significant repercussions on trade relations among its members and between them and the world[18]. In the spirit of the last courtiers of the Forbidden City, silence seems to be the best way out in the face of a reality that can no longer be controlled.

For ASEAN, responsible from the outset for the efficient conduct of the negotiations, the new pact multiplies partnerships, expands economic resilience, and promotes inclusive growth within the Association. As supervisor of the implementation of the RCEP, the ASEAN Secretariat monitors its execution, coordinates dispute resolution, facilitates necessary revisions, and keeps the RCEP aligned with the objectives of trade liberalization, economic cooperation, and the promotion of regional trade integration. The RCEP reinforces ASEAN's centrality in the Asian economic architecture and positions ASEAN as an indispensable trading platform.

BRAZIL IN THE GLOBAL CONTEXT

Brazil is one of the world's major economies. Since 1975, it has been among the ten largest global economies in terms of nominal GDP, with only three temporary interruptions–in the early 1980s, at the turn of the 2000s, and during the two-year period of the Covid-19 pandemic[19]. Outside of these intervals, it has consistently remained between fifth and tenth place worldwide, a consequence of the importance of its primary and industrial sectors in the formation of the national product. In purchasing power parity, Brazil currently ranks seventh in the world, reflecting the size of its domestic market and the relative purchasing power of its population.

The country occupies half of South America's area and accounts for half of its population; its GDP of approximately US$2.36 trillion is equivalent to half of South America's GDP. A major global exporter, it is the largest oil producer in Latin America. It exerts leadership in multilateral discussions on trade and combating climate change; it is a member of both BRICS and the G20; it is currently presiding over the World Climate Summit; and it is universally appreciated for its conciliatory tradition and capacity for negotiation and mediation.

In the WTO's global trade ranking, Brazil is among the 25 largest exporters. In terms of agricultural products, it is one of the three largest global exporters, rivaling the United States and the European Union as a major supplier of food to large Asian markets. The country is the leading global exporter of soybeans, coffee, sugar, orange juice, beef, and chicken.

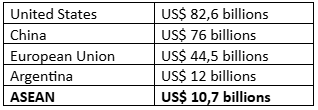

Commodities account for about 60% of Brazilian exports, with soybeans predominating as the main item (15% of external sales), followed by iron ore (12%, the second largest exporter in the world) and beef (6%)[20]. Manufactured products account for about 35% to 40% of exports, driven by sales of vehicles, the aerospace and defense (Embraer) sectors, and steel. Considering both goods and services, a comparison between Brazil's main trading partners in 2024, the last year for which complete data is currently available, shows the following results[21]:

Table 5 – Values in US dollars that Brazil imported from its main trading partners in 2024.

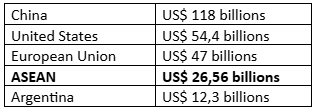

Table 6 – Values in US dollars that Brazil exported to its main trading partners in 2024.

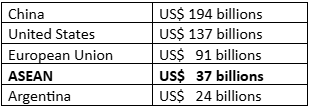

Table 7 – Trade flow (goods + services) between Brazil's main trading partners in 2024.

China, Brazil's main trading partner since 2009, absorbed almost 20% of Brazilian exports that year, resulting in a trade surplus for Brazil of around US$42 billion. Brazil's trade with China accounts for 85% of the combined trade with its next two partners, the US and the EU.

The United States, the second-largest partner, accounted for less than 10% of exports, with a deficit against Brazil of around US$ 28 billion, resulting from the import of manufactured goods, technology, and services such as royalties and profit remittances. Trade with the European Union totaled US$ 91.5 billion (15.3%), with a slight Brazilian surplus of US$ 2.5 billion.

Regarding ASEAN, the total trade flow, as observed, amounted to approximately US$ 37 billion, with a robust surplus of US$ 15.5 billion for Brazil (20% of the Brazilian trade balance surplus in 2024), placing the Association firmly among Brazil's top five trading partners (MRE 2025a; APEX Brasil 2025).

Brazilian foreign trade encompasses both strengths and vulnerabilities. While a solid commodity base sustains surpluses, greater diversification of the export portfolio is desirable to mitigate risks. A systematic policy of closer ties with ASEAN, coupled with initiatives in innovation, reindustrialization, and expanding trade partnerships, offers opportunities for Brazil to continue consolidating its global gains.

COMMERCIAL IMPORTANCE OF ASEAN FOR BRAZIL

ASEAN is emerging as a rapidly growing trading partner for Brazil. Trade (goods + services) increased from approximately US$3.5 billion in 2002 to US$37 billion in 2024, representing a more than tenfold increase in 22 years, driven by the competitiveness of Brazilian agribusiness and mining. Brazilian exports are concentrated in soybeans, iron ore, beef, sugar, and corn, with Indonesia and Malaysia being the main destinations for these products. Brazil imports from ASEAN primarily electronics and semiconductors (40%), machinery (25%), textiles (15%), and chemicals (10%).

Trade between Brazil and ASEAN has grown at an average of about 15% each year since 2020, contrasting with the relative stagnation of traditional markets.

Emblematic cases illustrate the supremacy of certain ASEAN members over Brazil's historical trading partners in Europe and Latin America. Driven by refined petroleum products and aircraft, exports to Singapore reached US$7.9 billion in 2024–more than Brazil exported to Germany (US$5.85 billion) and more than double what Brazil exported to France (US$3 billion).

In 2024, trade with Malaysia reached US$5.9 billion, with exports exceeding US$4.3 billion and a surplus for Brazil of US$2.8 billion. Brazilian sales were concentrated in iron ore (37%) and crude oil (28%). Brazil exported more to Malaysia in 2024 than to Italy, Portugal, the United Kingdom, or France (MRE 2025b).

Indonesia, with US$4.5 billion in purchases (soybeans and soybean meal), surpassed the United Kingdom (US$3.34 billion). Vietnam, with imports of US$4.2 billion (soybeans and pork), surpassed Peru (US$3.8 billion). Thailand, which bought US$3.45 billion from Brazil (ethanol and chicken), surpassed France (US$3 billion). These flows point to a diversified and resilient export portfolio, with room for significant expansion of Brazilian exports as ASEAN continues on its path towards ever greater affluence and development (MDIC 2024).

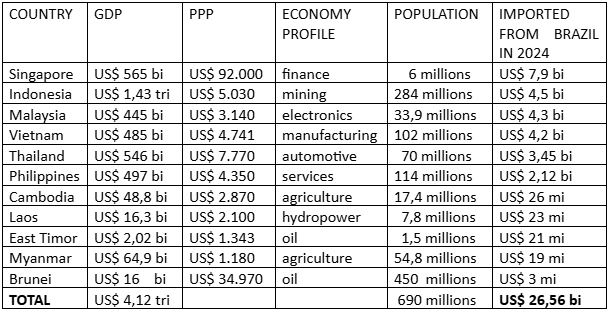

The table below shows the eleven members of ASEAN, with the enormous diversity of economic and demographic profiles that characterize them, presented in descending order of volume of imports of Brazilian products[22]:

Table 8 – ASEAN member countries in descending order of import volume of Brazilian products.

As discussed above, the ASEAN countries represent a consumer market of 690 million people for Brazil (three times the Brazilian population), increasingly affluent, with a combined GDP equivalent to almost twice the Brazilian GDP. In this dynamic environment, which is a powerhouse of wealth and trade generation, there is enormous room for expansion for the entry of Brazilian products, both manufactured and from agribusiness.

BRAZIL'S INTEREST LIES IN THE GROWING RAPPROCHEMENT WITH ASEAN.

The partnership between Brazil and the Association is not limited to trade. In 2022, Brazil obtained the status of ASEAN Sectoral Dialogue partner, which it shares with seven other countries[23] and which confers a welcome degree of political institutionalization to contacts with the region. In December 2023, an action plan for the Brazil-ASEAN partnership, entitled "Areas of Practical Cooperation 2024-2028," was adopted, defining concrete priorities for joint action. The plan's axes prioritize coordination across trade and investment, sustainable agriculture, energy transition, digital connectivity, climate change, and global governance.

Brazil is the only ASEAN Sectoral Dialogue partner in Latin America. It is the only Sectoral Dialogue partner to maintain a permanent representation, opened in March 2024, with the ASEAN Secretariat, based in Jakarta.

The status of Sectoral Dialogue partner should not be confused, however, with that of Dialogue partner, which is more complex and comprehensive, that ASEAN maintains with China and the United States, or Japan and the European Union[24]. Full dialogue (as opposed to sectoral dialogue, which focuses on specific topics) provides the partner country with participation in high-level forums, such as the annual ASEAN leaders' summits and ministerial meetings across various areas, as well as broad strategic cooperation.

President Lula invited the Prime Minister of Malaysia, Anwar Ibrahim, to participate in the G20 and BRICS Summits, which Brazil hosted in Rio de Janeiro in November 2024 and July 2025. Upon Malaysia assuming the rotating presidency of ASEAN, Anwar Ibrahim reciprocated the gesture–despite Brazil not being a full dialogue partner–by inviting Lula, in the capacity of Guest of the Chair, to take part in the Association's summit meeting held in Kuala Lumpur in October 2025.

The unprecedented participation of a Brazilian head of state in the 47th ASEAN summit is a historic advance in relations between Brazil and the Asian bloc. It constitutes an eloquent milestone in Brazil's political rapprochement with Southeast Asia. It was a high point in President Lula's foreign policy during his third term.

On the sidelines of the ASEAN summit (October 26), the president made bilateral state visits to Indonesia (October 23), the region's largest economy, and to Malaysia (October 25), a major investor in Brazil's oil and gas sector. In Jakarta, he visited the Association's headquarters, where he announced Brazil's interest in becoming a full dialogue partner of ASEAN and in increasingly close political and economic coordination. In Kuala Lumpur, as in Jakarta, much was said about expanding bilateral trade and investment volumes with Brazil, which are already significant.

The external observer sees the Association as a cohesive bloc, supported by a formidable network of ASEAN+1 trade agreements[25] and, more recently, by the comprehensive provisions of the RCEP. For third countries, the high degree of intra-ASEAN coordination, as well as that between ASEAN and its major Asian counterparts, presents both opportunities and challenges. By valuing inputs from any country in the bloc, not just the final producer, the RCEP's diagonal cumulativeness rule, as mentioned above, encourages the integration of internal production chains among the Parties. For an outside partner, there may be a risk of trade diversion, with reduced market access for actors outside the agreement; marginalization in global chains, with preference for regional inputs; and reduced competitiveness due to residual tariffs for non-members.

These issues reinforce, for Brazil as for any extra-regional partner, the need to mitigate risks in commercial relations with the Association. The path to concluding an agreement with ASEAN remains open, despite the complexities inherent in negotiations of this nature. Negotiations for a free trade agreement between ASEAN and the European Union were initiated, but due to limitations in its own internal coordination processes, the EU began to prioritize individual instruments with countries within the Association (EU-Singapore in 2019; EU-Vietnam in 2020). Formal discussions are underway between ASEAN and Canada and between ASEAN and the Gulf Cooperation Council. With MERCOSUR, an exploratory dialogue has been ongoing since 2007, without formal negotiations to date.

Brazil has, through the FTA between MERCOSUR and Singapore[26], signed in December 2023 and is still pending internalization by the Parties, a trade instrument with an ASEAN member state. Whether or not the opportunity arises in the future to launch negotiations for a trade agreement between the two regional blocs, it seems certain that Brazil has an interest in the growing consolidation of its formal ties with ASEAN.

Beyond deepening economic and commercial complementarities, which are clearly of mutual interest, there seems ample room to diversify opportunities and for Brazil to propose new areas of coordination with ASEAN–from economic and financial dialogue to coordination in multilateral forums and the promotion of concrete cooperation across various spheres.

PERSPECTIVES

In a scenario of rapid geoeconomic transformations and acute global geostrategic instability, characterized by the unpredictability of the United States' political and commercial actions toward traditional partners and historical allies–and amid the apparent apathy of European leaders–the interest of Brazil in reaffirming the strategic importance of Southeast Asia is undeniable.

The trade relationship between Brazil and ASEAN follows its own dynamics, dictated by Brazil's strong competitiveness and growing Asian demand. Brazil, on the other hand, stands to gain by also deepening its political relationship with the bloc, seeking to secure increasingly higher levels of structural alignment with the Association.

The arbitrary trade sanctions that Brazil and other major exporters have been subjected to underscore the urgent need to diversify export destinations. While continuing to cultivate its significant portfolio of trade and political relations with the United States, Europe, and its MERCOSUR neighbors, Brazil has much to gain by pursuing a systematic policy of rapprochement with Asia and, within Asia, with the ASEAN countries.

For Brazil, vital issues are at stake, such as market diversification, increased exports, including those with higher added value, reduced exposure to volatile markets, attracting investment, and technological cooperation. Despite potential challenges (such as competition in manufacturing sectors), Brazil will benefit from investing in closer dialogue with ASEAN, aimed at overcoming logistical barriers, harmonizing sanitary standards, resolving specific trade irritations, and developing economic diplomacy in its broadest sense.

One of the most economically dynamic regions in the world, whose economic and geographic position makes it the epicenter of emerging global economic and trade competition, ASEAN emerges as an indispensable partner in reorienting Brazil's international insertion. In a world that has evolved and continues to transform, the Brazil-ASEAN axis strengthens Brazil's economic sovereignty, promoting necessary inclusive growth in alignment with predictable and lasting South-South partnerships.

Notes

[1]The creation of the National Council for Industrialization, a state body for planning Brazilian industrial development, dates back to 1941. The same year saw the founding of the Companhia Siderúrgica Nacional (CSN) in Volta Redonda (RJ), which began receiving financing and technical support from the United States under the terms of the so-called Washington Agreements (1942). CSN was essential for Brazilian steel production, the basis for the national development of heavy industry.

[2]The American political scientist Francis Fukuyama (1992) argued, in The End of History and the Last Man, that so-called liberal democracy, associated with market capitalism, had definitively established itself as the dominant global model in a world that had overcome the Cold War.

[3]In *Capital in the Twenty-First Century*, French economist Thomas Piketty (2013) discusses the relative impoverishment of the American middle class in a context of increasing income inequality. In the third part of the work ("The Structure of Inequalities"), the author compares labor income and capital returns, diagnosing a trend in favor of the capture, by an increasingly smaller minority, of the benefits of the country's economic growth.

[4]The so-called Plaza Accord, signed in 1985 by the US, Japan, West Germany, France, and the United Kingdom at the Plaza Hotel in New York, promoted the coordinated devaluation of the dollar against the yen and the mark, with the successful aim of reducing in Japanese and German export competitiveness. In the same year, US sanctions against Toshiba considerably weakened the company, an emblem of the industrialization and internationalization of the Japanese economy, signaling a reduction in Japanese participation in the global trade of goods. The strategic autonomy of Japan and Germany is limited, as U.S. troops have remained stationed since the end of World War II. The same cannot be said of China, the main trading partner of most countries, which is impervious to strategies of this kind.

[5]As a result of the exacerbation of policies favoring the financial economy at the expense of the real economy, the 2008 crisis generated recession, unemployment, a drop in consumption, and a consequent reduction in American imports. The fall in production, credit, and investment, in turn, had a negative effect on US export performance.

[6]In the context of global trade in services, which is on the order of US$14 to 15 trillion (WTO and IMF, 2024 data), the US still leads, with about 17% of global trade, while China accounts for about 8%. China is making rapid advances in services, especially in digital services, engineering and logistics, and is increasingly investing in artificial intelligence, fintech and cloud computing.

[7]Industrial production is generally measured by what is called manufacturing value added (MVA), which captures the net value of goods produced. Data from the World Bank’s World Development Indicators, filtered by country and year, show China with an MVA of approximately US$4.66 trillion, compared to US$2.91 trillion for the US, around US$2.5 to 3.0 trillion for the EU, and around US$0.87 trillion for Japan (World Bank. World Development Indicators 2025).

[8]The 2025 annual edition of the Index of US Military Strength, published mid-year by the Heritage Foundation, a conservative American think tank specializing in defense and security, classifies US military power as "weak" for the second consecutive time, in contrast to Chinese advances in this area. Complementary analyses by the Heritage Foundation, released after the parade, refer to it as evidence of the "accelerated modernization" of the People's Liberation Army (PLA). The Heritage Foundation (2025).

[9]Hypersonic missiles and the so-called complete nuclear triad—nuclear bombers, intercontinental ballistic missiles (ICBMs), and submarine-launched ballistic missiles (SLBMs)—were all displayed in the parade.

[11]According to the IMF's World Economic Outlook, the Global South is projected to grow approximately 2.5-2.7 percentage points faster than the North in 2025-2026, and this difference is expected to remain stable in the medium term. The same projections indicate that, without major shocks, the GDP of the South (in PPP) will reach approximately 65% of the global total by 2030 (IMF 2025).

[12]In addition to the official languages, which may be three or four per country, more than a thousand other languages are spoken by the different ethnic groups in the member states. In Indonesia alone, with its 17,000 islands, around 700 languages are spoken.

[13]The free flow of labor is restricted to qualified professionals in specific sectors, which is regulated through mutual recognition agreements that prioritize the mobility of professionals in eight priority areas: medicine, dentistry, nursing, engineering, architecture, surveying, accounting, and tourism.

[14]The ASEAN Secretariat estimates in its Statistical Highlights, updated in 2024, that the Association's current nominal GDP would be between US$3.98 and 4.0 trillion (Source: ASEAN Secretariat 2024c).

[15]Here I used the Asian Development Outlook, published by the Asian Development Bank (ADB), which provides detailed GDP growth projections by country, extended, in some scenarios, to 2030 (ADB 2024, pp. 45-67 [for country projections] and p. 120 [for RCEP impact]).

[16]Manufacturing (30%) and tourism (5%-10%) are measured using the production method, which calculates each sector's contribution to GDP. Consumption (60%) and exports (40%) are components of GDP calculated using the expenditure method, which breaks down GDP into spending categories (consumption, investment, government, and net exports).

[17]India officially announced its withdrawal from the negotiations on November 4, 2019, during an ASEAN summit in Bangkok, Thailand. The announcement was made in the final stages of the agreement's conclusion, which was to be signed by the other negotiators on November 15, 2020. Among the reasons cited for the decision were India's trade deficit with China, domestic pressures due to fears of a negative impact on vulnerable sectors (agriculture, manufacturing), and the failure to obtain specific concessions for certain Indian services (IT and pharmaceuticals).

Less often noted is the fact that India was at that time being closely courted by the US, which wished to promote it as a pillar of an "Indo-Pacific" strategy (as opposed to the classic "Asia-Pacific" concept) for the region, in an effort that ultimately did not yield the expected results. India's withdrawal from the RCEP corresponded, at that moment, to a tacit alignment with American interests, especially amidst the US-China trade confrontation. Today, we see the arbitrary imposition of US tariffs on India, an India-Russia rapprochement driven by Indian acquisition of Russian energy, and India's pursuit of greater understanding with China. The withdrawal from the RCEP meant the loss for India of preferential access to important regional supply chains; the agreement leaves the door open for the country to rejoin in the future.

[18]“Civilizations die from suicide, not by murder,” said Arnold Toynbee in a well-known passage from *A Study of History* (1934, 38). The United States withdrew from the Trans-Pacific Partnership (TPP) negotiations in January 2017, originally conceived as a tool to contain China's commercial expansion. Now in the form of the Comprehensive and Progressive Agreement on Trans-Pacific Partnership (CPTPP), which it adopted after the surprising US withdrawal, this instrument was signed in 2018 and includes 11 countries (Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, Peru, New Zealand, Singapore, and Vietnam), seven of which are members of the RCEP. In 2021, China formally requested accession to the CPTPP, followed a few days later by Taiwan. The United States is not currently part of any significant formal economic arrangement in Asia.

[19]Between 1982 and 1984, during the external debt crisis and recession, Brazil fell to 11th-12th position, impacted by the debt crisis and recession. From 1999 to 2006, currency devaluation and low growth led the country to positions 11th to 14th. More recently, between 2020 and 2021, the COVID-19 pandemic and the depreciation of the real resulted in a drop to 12th-13th, temporarily interrupting the consistent trajectory among the top ten economies, which has been maintained since 1975, notably peaking at 5th position in 2011.

[20]In 2024, the eight main export products included crude oil, soybeans, iron ore and concentrates, sugar, processed petroleum oils, coffee, frozen beef, and undissolved chemical wood pulp (MDIC 2024).

[21]Sources: for the United States, MDIC (Comex Stat), Central Bank, Bureau of Economic Analysis (BEA); for China, MDIC (Comex Stat), Central Bank, General Administration of Customs of China; for the European Union, MDIC (Comex Stat), Central Bank, Eurostat; for ASEAN, MDIC (Comex Stat), Central Bank, IBRE/FGV; for Argentina, MDIC (Comex Stat), Central Bank, INDEC.

[22]Sources: for GDP and GDP per capita, IMF and World Bank estimates for 2025; for trade volumes (MDIC 2024).

[23]The following are the other partners in sectoral dialogue with ASEAN: South Africa, United Arab Emirates, Morocco, Norway, Pakistan, Switzerland, and Türkiye.

[24]The following are the partners in full dialogue with ASEAN: Australia, Canada, China, South Korea, the United States, India, Japan, New Zealand, the United Kingdom, Russia, and the European Union.

[25]In descending order of effective date: ASEAN-Hong Kong Free Trade Area; ASEAN-India Free Trade Agreement; ASEAN-Australia-New Zealand Free Trade Area; ASEAN-Japan Comprehensive Economic Partnership; ASEAN-South Korea Free Trade Area; ASEAN-China Free Trade Area; and the ASEAN Free Trade Area proper.

[26]The first FTA to be concluded between MERCOSUR and one of the ASEAN member states. A Comprehensive Economic Partnership Agreement (CEPA) between MERCOSUR and Indonesia and an FTA between MERCOSUR and Vietnam are currently under negotiation.

References

ApexBrasil. 2025. Perfil de comércio e investimentos ASEAN 2024. Brasília: ApexBrasil. https://apexbrasil.com.br/content/apexbrasil/br/pt/solucoes/inteligencia/estudos-e-publicacoes/perfil-de-comercio-e-investimentos/perfil-de-comercio-e-investimentos---asean---2025.html.

ASEAN Secretariat. 2024a. ASEAN Statistical Highlights 2024. Jakarta: ASEAN Secretariat, 2024.

ASEAN Secretariat. 2024b. ASEAN Merchandise Trade Statistics 2024. Jakarta: ASEAN Secretariat.

ASEAN Secretariat. 2024c. ASEAN Key Figures 2024. Jakarta: ASEAN Secretariat. https://asean.org/serial/asean-key-figures-2024/.

ASEAN Secretariat. 2024d. “Top 10 News Stories on 2024 China-ASEAN Cooperation”. Jakarta: ASEAN Secretariat, December 31, 2024.

Asian Development Bank (ADB). 2024. Asian Development Outlook 2024: Fiscal Policy for Inclusive and Sustainable Growth. Manila: Asian Development Bank. https://www.adb.org/outlook/editions/april-2024.

Bown, Chad P. 2021. The Regional Comprehensive Economic Partnership: Why It Matters and What It Means. Washington, DC: Peterson Institute for International Economics.

Eurostat. 2025. Eurostat Database. Luxembourg: European Commission.

Fukuyama, Francis. 1992. The End of History and the Last Man. New York: Free Press.

General Administration of Customs of the People's Republic of China. 2025. China Customs Statistics. Beijing: General Administration of Customs.

Heritage Foundation. 2025. 2025 Index of US Military Strength. Washington, DC: Heritage Foundation. https://www.heritage.org/military-strength.

Instituto Brasileiro de Economia. 2025. IBRE Data Portal. Rio de Janeiro: Fundação Getúlio Vargas.

Instituto Nacional de Estadística y Censos (INDEC). 2025. Buenos Aires: Ministerio de Economía.

International Monetary Fund. 2025. World Economic Outlook: Global Economy in Flux, Prospects Remain Dim. Washington, DC. https://www.imf.org/en/publications/weo/issues/2025/10/14/world-economic-outlook-october-2025.

Kissinger, Henry. 2011. On China. New York: Penguin Press.

Lins, Álvaro. 1995. Rio Branco: Biografia Pessoal e História Política. São Paulo: Alfa Omega.

Mahbubani, Kishore. 2022. The Asian Twenty-First Century. London: Springer Nature.

Mahbubani, Kishore. 2008. The New Asian Hemisphere: The Irresistible Shift of Global Power to the East. New York: Public Affairs.

Mahbubani, Kishore & Jeffery Sng. 2017. The ASEAN Miracle: A Catalyst for Peace. Singapore: National University of Singapore. https://doi.org/10.2307/j.ctv1xz0m3.

Ministério do Desenvolvimento, Indústria, Comércio e Serviços (MDIC). 2024. Comex Stat: Balança Comercial Brasileira. Brasília: MDIC.

Ministry of Commerce of the People’s Republic of China (MOFCOM). 2025. “China-ASEAN Trade Reaches 6.99 Trillion Yuan in 2024.” Beijing: MOFCOM, January 15, 2025.

Ministério das Relações Exteriores. 2025a. "Visita do Senhor Presidente da República à Malásia". Gov.br, Nota à Imprensa 500, 25 de outubro de 2025. https://www.gov.br/mre/pt-br/canais_atendimento/imprensa/notas-a-imprensa/visita-do-senhor-presidente-da-republica-a-malasia.

Ministério das Relações Exteriores. 2025b. "Participação do Senhor Presidente da República na 47ª Cúpula da Associação de Nações do Sudeste Asiático (ASEAN) e na 20ª Cúpula do Leste da Ásia". Gov.br, Nota à Imprensa 505, 25 de outubro de 2025. https://www.gov.br/mre/pt-br/canais_atendimento/imprensa/notas-a-imprensa/participacao-do-senhor-presidente-da-republica-na-47a-cupula-da-associacao-de-nacoes-do-sudeste-asiatico-asean-e-na-20a-cupula-do-leste-da-asia.

National Science Foundation. 2025. “Long-Term Trends Show Decline in Federally Funded R&D as a Share of GDP while Business-Funded R&D Share Increases.” NSF, 25 (334). https://ncses.nsf.gov/pubs/nsf25334.

Piketty, Thomas. Le Capital au XXIᵉ siècle. Paris: Seuil, 2013.

Shatz, Howard J. 2023. Assessing the Regional Comprehensive Economic Partnership (RCEP): Implications for US Interests. Research Report RRA2080-1. Santa Monica, CA: RAND Corporation.

Petri, Peter A. & Michael Plummer. 2020. “RCEP: A New Trade Agreement That Will Shape Global Economics and Politics.” Brookings Institution, November 16, 2020. https://www.brookings.edu/articles/rcep-a-new-trade-agreement-that-will-shape-global-economics-and-politics/.

Toynbee, Arnold. 1934. A Study of History. Oxford: Oxford University Press.

US Census Bureau & Bureau of Economic Analysis (BEA). 2025. “US International Trade in Goods and Services, December and Annual 2024.” Washington, DC: US Government Publishing Office. https://www.bea.gov/news/2025/us-international-trade-goods-and-services-december-and-annual-2024.

United Nations Conference on Trade and Development. 2025. Global Trade Update: October 2025. Geneva: UNCTAD.

World Bank. 2025. World Development Indicators. 2025. Washington, D.C.: World Bank. https://data.worldbank.org/indicator/NV.IND.MANF.CD.

World Intellectual Property Organization. 2024. World Intellectual Property Indicators 2024: Highlights. Geneva: WIPO.

World Trade Organization. 2025. World Trade Statistical Review 2025. Geneva: WTO.

Submitted: November 5, 2025

Accepted for publication: November 5, 2025

Translated by Victoria Corrêa do Lago with the support of digital machine translation tools: Google Translate (initial draft), Grammarly (grammatical and syntactic revision), and ChatGPT (selective phrasing refinements). Reviewed by the author.

Copyright © 2026 CEBRI-Journal. This is an Open Access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original article is properly cited.